Coronavirus, Pandemic, Quarantine, Social Distancing, …

Fourth Quarter 2020

It is safe to say that when the year started, few were thinking about words and phrases such as those above. We knew however, that 2020 was an election year, with all the fanfare, hyperbole and at times disingenuousness that is part and parcel of American politics. In general, political risk – potential changes in the value of financial instruments due to changes in political party or policy – is not something that investors spend too much time focused on. Administrations come and go and it is our opinion that the impact on the financial markets from political changes are largely short-term events. Only in hindsight are economists able to truly measure the impact of new policies. For example, a decade after the Great Recession, regulation meant to protect the financial system has only served to make the large U.S. banks more dominant than ever.

That said, the Federal Reserve, an unelected committee, has had a remarkable impact on investors’ expectations for decades, and since the Great Recession, it has been argued that the Fed’s ultra-loose monetary policy has pushed investors into risker assets, thereby driving up their prices and possibly distorting financial markets. As we have noted in prior quarterly commentaries, the Fed has spent trillions of dollars this year buying bonds of all types. The Fed recently changed its ‘framework’ for fighting downturns like the one we are currently in; it will wait for inflation to actually arrive, as opposed to potentially arrive, before raising interest rates. This implies that interest rates will stay lower, for longer, suppressing the return on cash and other safe assets.

As we check off the days in the final calendar quarter of a year that has been at times chaotic, unsettling and even frightening, we are faced with:

- An economic recovery that is stalling as the early gains from reopening the states and the broader economy recede,

- A stock market that has lost direction after hitting all-time highs earlier in the summer,

- Continued questions regarding the potential reacceleration of the virus during the winter months and the timing, distribution and efficacy of any vaccine(s), and

- A polarizing election, the outcome of which may not be known on November 3rd.

Investors and markets do not like uncertainty. In 2000, the stock market declined 7% waiting for results from Bush vs Gore. In the event of another contested election, it is reasonable to expect stock market volatility in November. Given two possible outcomes:

- If President Trump is reelected, we anticipate investors will quickly return their focus to the virus, vaccines, the outlook for corporate earnings in 2021, and ongoing tensions with China (and its impact on trade, protectionist policies and globalization).

- If Vice-President Biden wins, and the Democrats take control of the Senate, it is reasonable to expect tax increases for both corporations and individuals that some on Wall street would view as negative for stock prices. This could be offset, however, by infrastructure spending, higher minimum wages, or other spending plans that could provide an economic boost.

We contend, therefore, that the political landscape is a short-term sideshow and that the key is controlling the virus – potential economic growth, and therefore potential stock market growth, in 2021 and beyond, hinges on it.

Beyond the election and any potential transition in Washington, there are important longer-term questions that we believe investors need to be thinking about over the coming years:

- Will the virus alter consumer behavior, temporarily or permanently, including where people choose to live and work and how they choose to shop and spend,

- Which industries or sectors are the potential winners in a changed world,

- What is the future size and role of government, and

- Can the U.S. (or any developed country) grow at a sufficient pace in the future to reduce its unprecedented level of debt (Japan has shown this is easier said than done).

As part of our normal and ongoing asset allocation and portfolio management process, Mitchell Sinker & Starr’s Portfolio Managers will be reflecting on these topics and how they might impact client accounts and influence investment decisions going forward.

Economic and Capital Markets Data

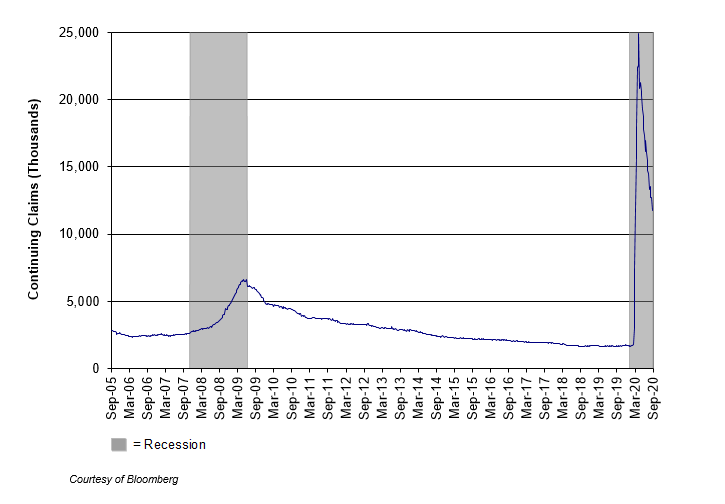

U.S. Continuing Jobless Claims – Fifteen Years

After peaking in May, continuing jobless claims have declined by roughly half, but remain at extremely elevated levels.

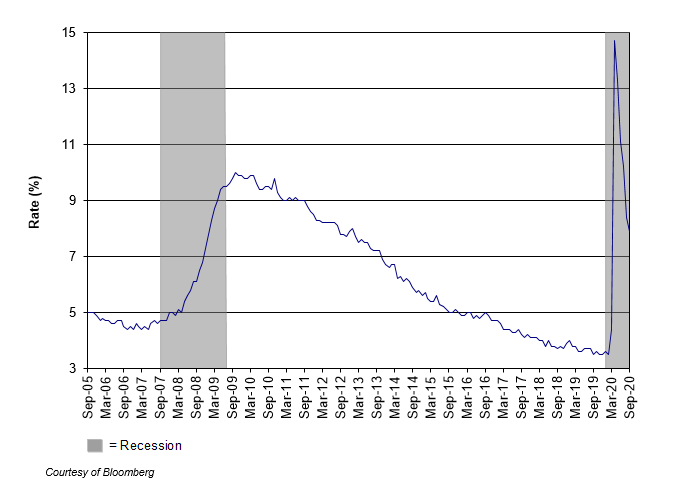

U.S. Unemployment Rate – Fifteen Year

As continuing claims have come down, so has the unemployment rate.

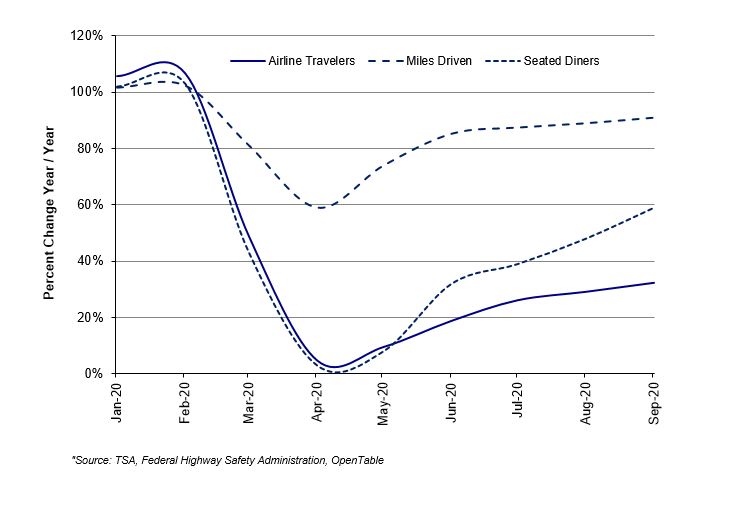

Alternative Data Points – Year-to-date

A variety of data sets confirm that in general, the initial pace of the economic recovery that began last spring has subsequently slowed.

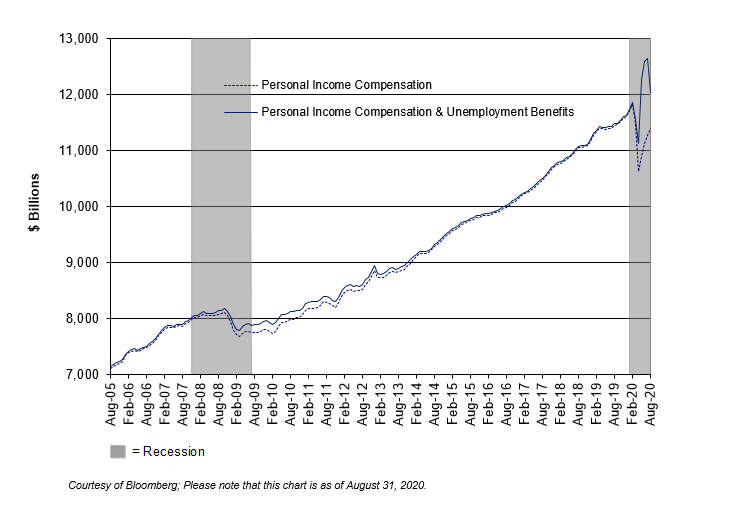

Total U.S. Monthly Compensation & Unemployment Benefits – Fifteen Years

Unlike previous downturns, Government unemployment and stimulus benefits have been so significant in 2020 that they initially increased total employee compensation. These payments began to decline in August.

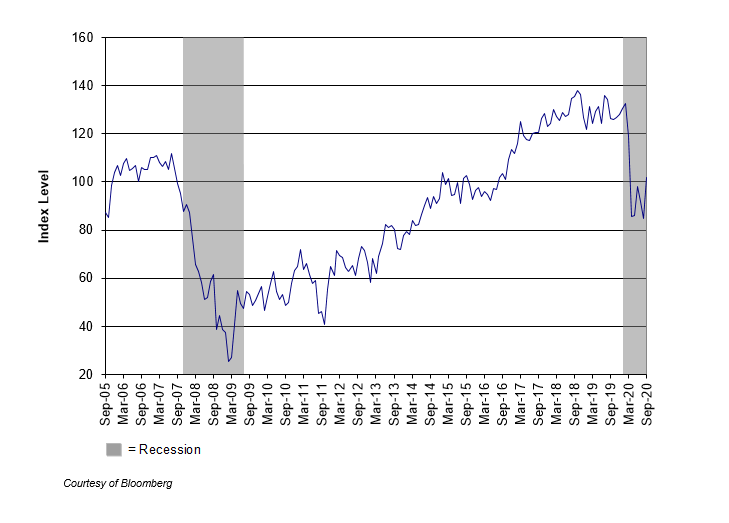

Consumer Confidence – Fifteen Years

Consumer confidence is still significantly higher than it was during the depths of the Great Recession. This may be attributed to both increased government benefits as well as expectations that a viable vaccine will help the economy recover quickly.

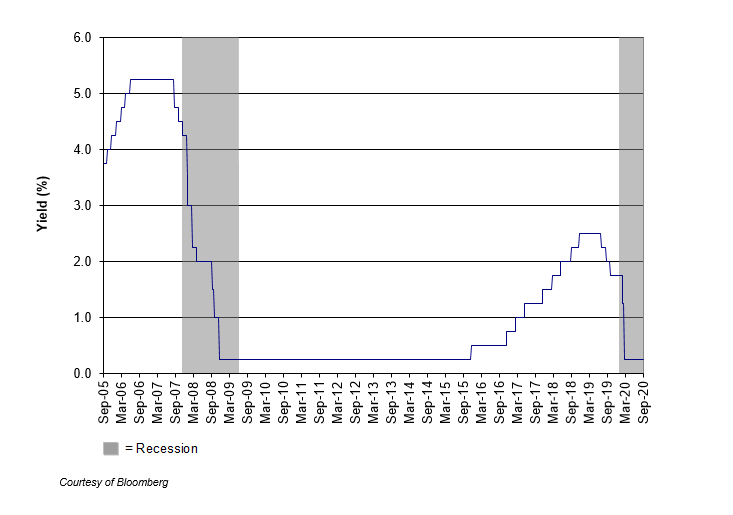

Federal Funds Target Rate – Fifteen Years

The Federal Reserve is committed to keeping interest rates low until inflation picks up.

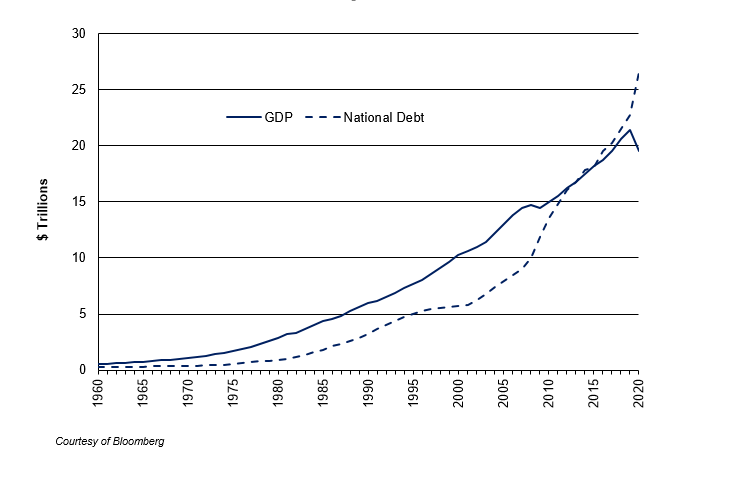

U.S. GDP vs. National Debt – Sixty Years

Total U.S. national debt has rapidly overtaken aggregate gross domestic product (GDP) during the downturn.

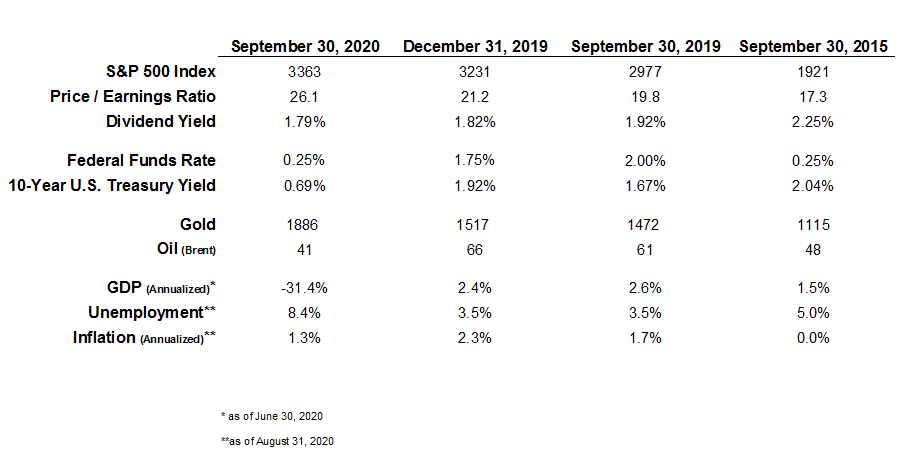

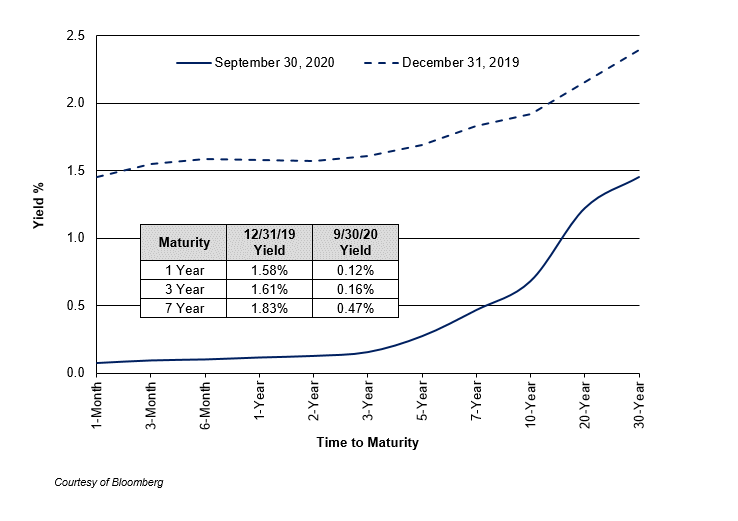

U.S. Treasury Yield Curve – Year-to-Date

The yield curve – interest earned on Treasury bonds at various maturities – has collapsed to new lows since start of the year.

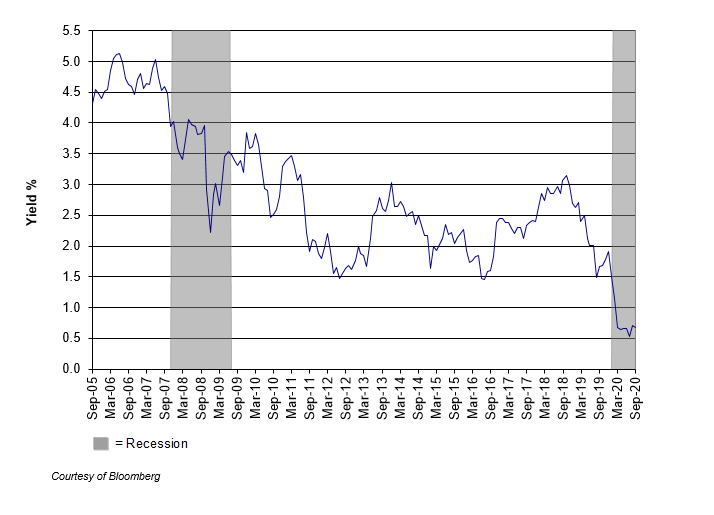

U.S. 10-Year Treasury Yield – Fifteen Years

In reaction to the economic impact of the virus, yields collapsed. This simply amplified the long-term trend of lower interest rates.

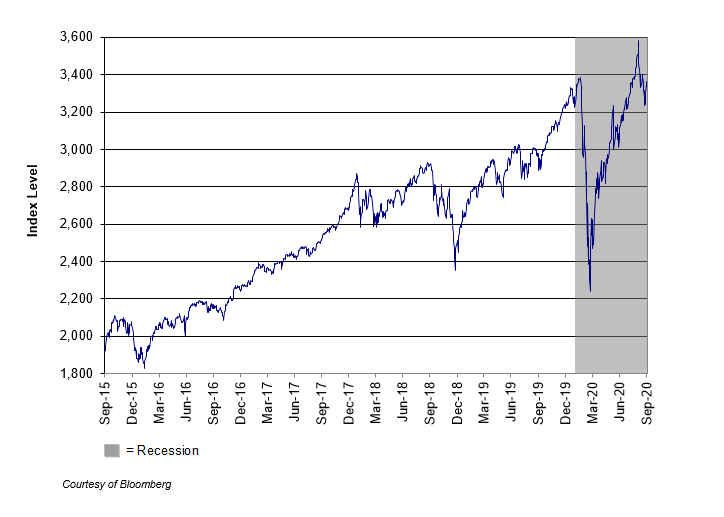

Standard & Poor’s 500 Index – Five Years

The rapid recovery in stocks has been surprising, considering the possible longer-term damage done to the underlying economy.

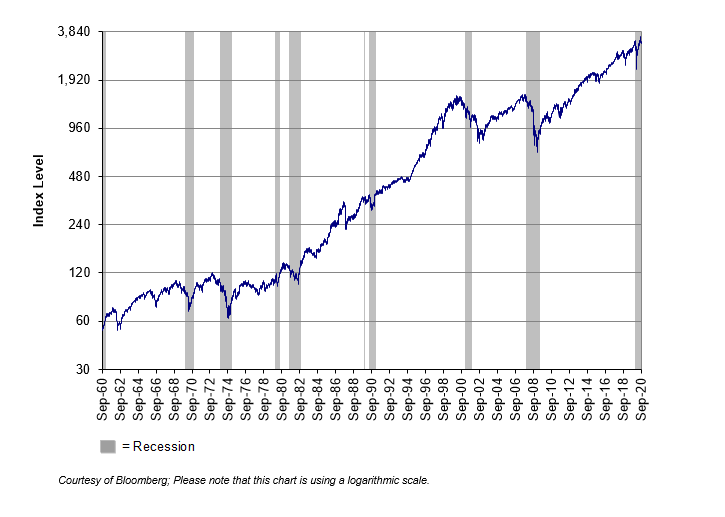

Standard & Poor’s 500 Index – Sixty Years

Over the long-term, stocks remain the only liquid asset class with the potential for growth in excess of inflation.

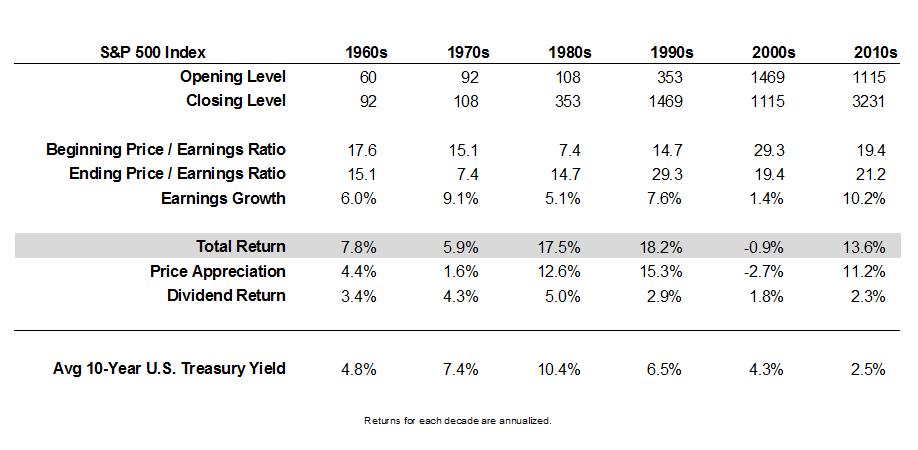

Financial Market Data – Decade-by-Decade